These last months have been a steep downward ride for oil prices accompanied with both euphoric and panic reactions. Many creative theories are circulating, each of them adding a little more geopolitical plotting to the previous one. However, the reason behind this fall can mainly be explained with simple supply and demand economics.

{kind=link}

Brent crude oil price since summer 2014

The article is published in Dutch by ‘Knack‘ and ‘KU Leuven blogt’.

Increased energy efficiency combined with slowing global economic growth and growth of alternative energy sources have tempered global demand of oil. The International Energy Agency (IEA) had to cut its growth forecast of worldwide consumption to 0.9 mb/d* in 2015, resulting in a total demand of 93.3 mb/d [1]. On the supply side however, production has grown substantially mainly due to America’s shale oil boom, rapidly transforming it from an importer country to a self sustaining superpower. The share of America’s shale industry in the international oil market has indeed increased with 2.2%-pts between 2008 and today, which is no surprise since e.g. last year shale accounted for at least 20% of worldwide oil production investments [2]. Combined with the unwillingness of the Organization of the Petroleum Exporting Countries (OPEC), a group of oil producers responsible for 40% of the world supply, to stabilize oil markets by cutting production, with growing production in Iraq and with relatively steady production in Russia, this resulted in a serious oil oversupply triggering a plunge of the price which has been cut in half since June 2014, reaching levels comparable to the 2009 recession.

However, disagreement reigns in the OPEC. On one side, several members like Iran, Venezuela and Algeria, with a government income highly sensible to the oil price, have urged the group to cut production in order to raise and stabilize the oil price. On the other side, Saudi Arabia and its Gulf state allies are standing firm with the consequences of the first oil crisis still in memory in order to avoid losing market share which would merely benefit their competitors.

The consequences of the sudden price drop are varied, both positive and negative.

Consumers are spoiled by savings at the pump. For an average American household this results in about 800$ less spending per year – equivalent to a 2% pay rise. Countries like Indonesia, India and Egypt are taking advantage of the low price to cut government fuel subsidies [3]. Doing so, they free government funds and will be able to increase spending on social projects. Kuwait will take even bolder steps as it plans to triple the price of diesel and kerosene in 2015.

Producers, on the other hand, are facing consequential drops in profits and consequently reduce capital spending. Big oil producing companies come under increased pressure as the oil they pump is being sold well below the expected price.

For the fourth quarter of 2014, BP reported a net loss of $4.4 billion and Shell reported a drop of 15% in total revenue, mainly because of the falling oil price [4] [5]. Other oil and gas producers like Exxon Mobil and Total are also taking hits [6] [7]. But it doesn’t stop here. Most of these companies reduce their capital spending because of estimated lower returns. Projects involving more difficult production are cancelled or postponed, reducing job opportunities and regional investments. Less exploration today will result in less production tomorrow, naturally pushing prices up again.

Producing countries highly dependent on their oil income are facing severe budgetary challenges which eventually could be paired with political and social turbulence. According to the World Bank, Russia’s economy, who’s export income consists for 70% of oil and gas revenues, faces a contraction of 0.7% in 2015 if the price of oil does not recover. The BBC reports that Russia loses about $2 billion in revenues for every dollar fall in oil price [8]. Saudi Arabia, the leading member of the OPEC, has made clear that it will tolerate the lower prices in order to do to shale firms’ finances what fracking does to rocks [2]. Indeed, Saudi Arabia has reserves that can be extracted relatively cheaply compared to the shale technology. The country can therefore take a temporary beat. The combination of an oil price under the breakeven price of the shale industry (today about $57 per barrel, according to IHS, a research firm) and the debts still piling up from previous investments in new drillings is likely to launch a rash of bankruptcy. That in turn would temporarily bespatter shale oil’s reputation amongst investors. Since shale oil wells are short lived, any slowdown in investment will quickly result into shrinking production [9]. However, shale drillers hold the advantage compared to companies exploring large scale untapped oilfields that their investments come in small increments. Drilling a new shale well costs about $1.5 million and can be completed in about a week, while e.g. Exxon Mobil and Rosneft recently spent 2 months and $700 million to drill a single well in the Kara Sea. Shale drillers can relatively easily adapt their exploration for new production to short term market prices. They might suffer a setback by the end of 2015, but they will easily find new investors in America’s risk-hungry capital markets and recover quickly with greater efficiency.

Additionally, a low oil price is bad news for our environment. It reduces the need to invest in renewables and energy efficient machinery on the short term. For instance, cheap jet fuel enables enormous operational savings for many airlines but could prompt them to reduce investment in new carriers with cleaner engines [10]. Cheaper gasoline provides less incentive to consumers to buy a more expensive but less polluting car.

{kind=link}

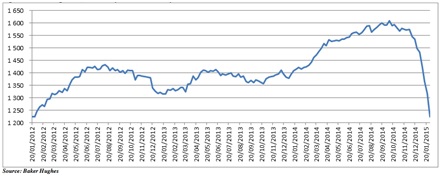

Shale rig count in US between 01/2012 and 01/2015

With reports of decreasing numbers of shale rigs in the U.S, the Brent price rose back from under $50 to just over $60. However, analysts remain skeptical. Last Friday, Bank of America Merrill Lynch still estimated global supply to run 1.4 mb/d above global demand. It speculates Brent will trade under $40 before an equilibrium between supply and demand will be reached.

Between speculations and actual supply and demand dynamics and with the perspective of a temporary decrease in investments in oil production and exploration and the already decreasing number of shale wells, it is reasonable to believe oil prices will gradually climb back but it’s impossible to accurately project its next stabilizing price. Much will depend on the technological progress in shale technology, the overdue implosion of Putin’s kleptocracy, the lasting unity of the OPEC and the future economic growth rate of our planet.